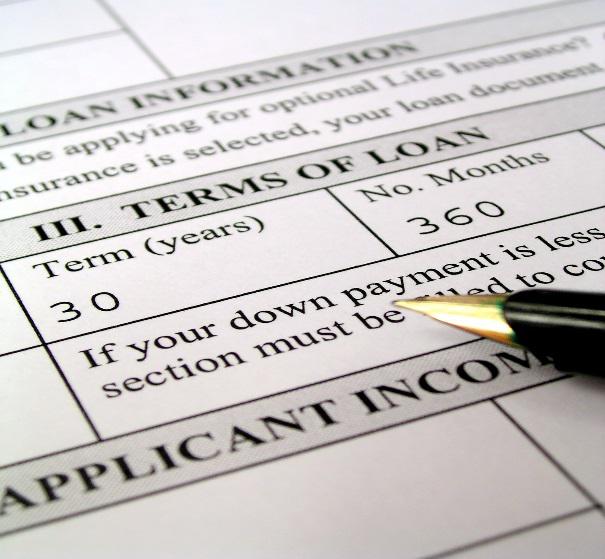

A loan modification can be defined as an agreement between a homeowner and a financial institution that changes the terms of the original mortgage loan. Homeowners who have fallen behind on their mortgage payments or who are having financial difficulties should seek to modify their mortgage loan for the purpose of obtaining a reduction of their mortgage payments that fits into their financial circumstances. It should be noted that a loan modification application does not stop a foreclosure lawsuit from moving forward. Whenever a homeowner is sued in a foreclosure lawsuit they must file a written Answer to the Summons and Complaint with the court and with opposing counsel within twenty days if served personally and thirty days if served by any other means. Failure to submit an Answer, even if a mortgage modification application is submitted, is considered a default and an admission of the allegations in the lawsuit which allows the lawsuit to move forward unopposed.

A loan modification can be defined as an agreement between a homeowner and a financial institution that changes the terms of the original mortgage loan. Homeowners who have fallen behind on their mortgage payments or who are having financial difficulties should seek to modify their mortgage loan for the purpose of obtaining a reduction of their mortgage payments that fits into their financial circumstances. It should be noted that a loan modification application does not stop a foreclosure lawsuit from moving forward. Whenever a homeowner is sued in a foreclosure lawsuit they must file a written Answer to the Summons and Complaint with the court and with opposing counsel within twenty days if served personally and thirty days if served by any other means. Failure to submit an Answer, even if a mortgage modification application is submitted, is considered a default and an admission of the allegations in the lawsuit which allows the lawsuit to move forward unopposed.

Various Mortgage Modifications

There are a variety of ways in which a mortgage can be modified. Examples of the types of manners in which a mortgage can be modified are as follows:

- The interest rate can be reduced.

- Payment terms, which are usually over a thirty year period, can be extended to as long as forty years.

- The arrears on the mortgage can be placed at the end of the mortgage and the payment terms extended by the amount of months in which payments were missed.

- Penalties and attorneys fees concerning the mortgage can be waived.

- Interest and late fees concerning the mortgage payments can be waived.

- An adjustable rate mortgage can be converted to a conventional mortgage.

- An adjustable rate mortgage can be converted into an interest only mortgage or a fixed rate mortgage.

All of the aforementioned ways of modifying a mortgage can be used individually or in combination with each other to create a lower cost, more affordable, monthly mortgage payment for the beleaguered homeowner.

Elliot S. Schlissel is a foreclosure attorney representing homeowners throughout the New York Metropolitain area.

In a case before Justice Yvonne Lewis sitting in the Supreme Court Foreclosure Part in Kings County, defendant Ellery Beaver LLC brought an application for summary judgment seeking the discharge of HSBC’s mortgage on their property. HSBC brought a cross application for dismissal of the action by the plaintiff.

In a case before Justice Yvonne Lewis sitting in the Supreme Court Foreclosure Part in Kings County, defendant Ellery Beaver LLC brought an application for summary judgment seeking the discharge of HSBC’s mortgage on their property. HSBC brought a cross application for dismissal of the action by the plaintiff.

The Consumer Financial Protection Bureau is reviewing new regulations which will put the brakes on a contentious practice called mandatory arbitration. Under mandatory arbitration rules, consumers must take disputes they have with financial institutions to third party mediators. This prevents them from going into courts and presenting their issues to judges. Consumer advocates feel this practice benefits large financial institutions, credit card issuers and financial service providers to the detriment of consumers.

The Consumer Financial Protection Bureau is reviewing new regulations which will put the brakes on a contentious practice called mandatory arbitration. Under mandatory arbitration rules, consumers must take disputes they have with financial institutions to third party mediators. This prevents them from going into courts and presenting their issues to judges. Consumer advocates feel this practice benefits large financial institutions, credit card issuers and financial service providers to the detriment of consumers. Justice Phyllis Orlikoff Flug sitting in a Foreclosure Part in Queens County Supreme Court recently had a case where the defendants moved to dismiss the bank’s lawsuit in a foreclosure legal action. The lawsuit had been initiated against the defendants Michael Pertab and Cholying Pertab in 2010. Michael had been served by personal service in July 2010 and Cholying had been served by substituted legal service in August 2010.

Justice Phyllis Orlikoff Flug sitting in a Foreclosure Part in Queens County Supreme Court recently had a case where the defendants moved to dismiss the bank’s lawsuit in a foreclosure legal action. The lawsuit had been initiated against the defendants Michael Pertab and Cholying Pertab in 2010. Michael had been served by personal service in July 2010 and Cholying had been served by substituted legal service in August 2010.